Employees Deposit Linked Insurance Scheme (EDLI Scheme)

Table of Contents

In the year 1976, the Indian Government launched a new insurance cover provided by the Employee’s Provident Fund Organization (EPFO), known as Employees Deposit Linked Insurance Scheme (EDLI). Life by itself is a mystery and very unpredictable. And this scenario has indispensably given rise to individuals enrolling for an insurance policy to make sure that their loved ones are secured. But unlike the public sector workforce, private sector employees are not entitled to many privileges.

Hence, the significant objective of EDLI is to provide social security and expand employee life insurance benefits to facilitate and financially support the dependents in times of any uncertainty that may arise. Under this scheme, the nominee of the employee is entitled to a lump-sum amount of up to ₹ 6 lakhs in case of the death of the EDLI member during his service period.

The EDLI scheme works in combination with EPF and EPS, thus making it mandatory for any organization registered under the Employee Provident Fund and Miscellaneous Provisions Act, 1952, to enroll for Employees Deposit Linked Insurance Scheme. The extent of benefit to this scheme is decided on the basis of the employee’s last drawn salary. The EDLI scheme is also transferable, i.e., in case the employee shifts to a new job, his EDLI account can be transferred too, and the employer can continue contributing to the employee’s existing account.

New Update

The year 2020 has become challenging for every individual. The pandemic has created such a precarious atmosphere worldwide that each one is worried and confused about the new normal that is remote working and how he can secure things for himself and the family. In this crisis, also an extended benefit under EDLI was brought forth by the Employees’ Provident Fund Organization.

In the month of September 2020, The Central Board of Trustees of EPFO approved an amendment of paragraph 22(3) of the EDLI scheme to enhance the maximum assurance benefit to ₹7 lakhs from the present benefit of ₹6 lakhs, mentioned the ministry of labour and employment in a statement. (Although the update is almost accepted, it’s still a matter of discussion)

The Features of EDLI

Some of the notable and salient features of Employees Deposit Linked Insurance Scheme are as follows:

- EPFO members are automatically enrolled for EDLI.

- The employee need not contribute to this scheme.

- The EDLI benefit can be claimed by the nominee, legal heir, or family member.

- The coverage under this scheme is available only as long as the employee is an active member of EPF.

- Under this scheme, a bonus of about 2,50,000 is applicable.

- The employer’s contribution should be 0.5% of the basic salary or a maximum of ₹ 75. The contribution is made on behalf of the employer by the human resource department during the payroll process.

- Under Section 17 (2A), if the employer wishes, he can opt for any other insurance scheme but must make sure that the benefits covered should be equivalent or more than the EDLI scheme.

- For registered employees, comprehensive insurance coverage is provided round the clock under the EDLI scheme.

- To avail EDLI benefits, no minimum service period is required.

- If the insured person dies during his active service period, the nominee mentioned in the document can claim the amount.

- The EDLI proceeds will be given to the legal heir in case the nominee is not mentioned or if the nominee doesn’t claim.

Eligibility Criteria For EDLI Scheme

It’s simplified. There are only two criteria to fulfill in order to enroll and avail coverage under EDLI. Here they are:

- The employee’s basic salary should be 15000. If the basic salary is more than 15000, then the maximum benefit coverage amount is limited to ₹ 6 lakhs.

- The organization that the employee is working for should have at least 20 workforces.

Contribution And Calculation Of EDLI

The EDLI scheme doesn’t require any contribution from the employee. But it’s the employer who is the contributor. This contribution is made along with the EPF, based on the Basic salary + Dearness allowance. The bifurcation is shown below:

| Employer | Employee | ||

|---|---|---|---|

| EPF | 3.67% | 12% | |

| EPS | 8.33% | – | |

| EDLI | 0.5% (Max-75) | – | |

The insurance amount is calculated as 30 times the average monthly salary in the last 12 months of employment. Which can be formulated as,

Average Monthly Salary x 30 + Bonus Amount

Whereby,

– The average salary of the insured may be capped up to 15,000 per month.

– Therefore, amounting 7 lakhs as the maximum coverage to be paid under the EDLI scheme.

The contribution is made during the payroll process, depending on the organization’s policy.

What Are The Prerequisite Documents?

To claim the insurance amount, the claimant is required to submit the following documents.

- Form 5

- Death certificate of the insured

- A cancelled cheque of the bank account details

- In case the insured is a minor family member, the legal guardian has to submit the ‘Guardianship Certificate.’

- If the nominee is not mentioned during the registration, then the legal heir has to submit the ‘Succession Certificate’ to claim the insurance amount.

- In case the EDLI member was employed in an organization exempted under the EPF scheme 1952, the employer should furnish the last 12 months’ PF details under the certificate part along with the attested copy of the Insured’s Nomination Form.

How To Claim The EDLI Benefits?

As mentioned earlier, the nominee mentioned in the document has to claim the EDLI. In case there if the nominee is not specified, the legal heir or one of the family members can put forward the claim. The insured member, being an active EPF member at the time of uncertainty, is mandatory.

The steps in claiming the insured amount by the nominee are as follows:

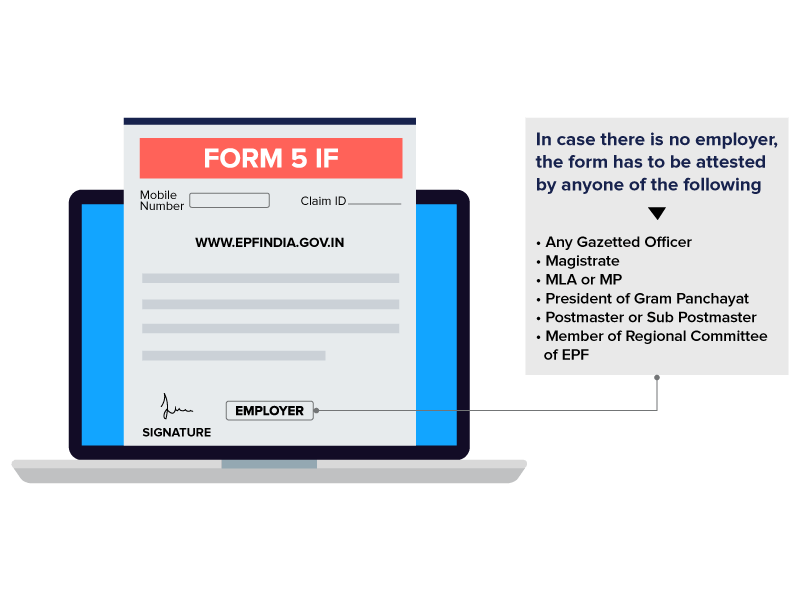

- Firstly, the nominee has to fill and submit the Form 5 of EDLI.

- The filled form has to be certified and signed by the employer.

If at all, getting the Form certified and approved by the employer isn’t possible, along with Form 5, any of the following can be attested-

– Local MLA or MP

– Gazetted Officer

– Bank Manager (in the branch where the insured account was maintained)

– Postmaster or Sub Poster

– Magistrate

– President of Village Panchayat

– Member of CBT or Regional Committee of EPF - Once Form 5 is signed, it must be submitted along with the other necessary documents to the EPF Commissioner Office for the further process to begin. (If needed, the claimant can also submit Form 20 (EPF withdrawal claim) and Form 10C/D to claim the valid benefits under the schemes EPS, EPF, and EDLI).

- All these submissions are to be furnished as early as possible so that there is no delay in the process.

- The EPF Commissioner, on the receipt of all the required documents, has to settle and disburse the claim amount to the nominee within 30 days of the Form submission. If failed, the claimant will be entitled to 12% of interest per annum till the date of the beneficiary amount settlement.

Is there an Alternative for Employees Deposit Linked Insurance Scheme?

Surely there are. As mentioned in the features, if an employer wishes to choose any other group insurance scheme apart from the EDLI, he can. But, under the condition that the benefits covered by the scheme chosen should be equivalent to or more than that of the EDLI. In recent days, many group life insurance terms have come up offering better benefits to the employees. And therefore, many private employers and employees opt for them. Some of these alternatives include:

- LIC Group Insurance Scheme

- HDFC Life Group Term Insurance Plan

- Max Life Group Super Life Premiere

Conclusion

In the present scenario, it’s mandatory that the employers fulfill the social responsibility towards their stakeholders. And the employees are also called the first customers; hence, making them feel secure is a major issue. The EDLI scheme provides an opportunity to secure the employees to a certain extent, and it offers benefits that are worth opting for. Therefore, It will be a wiser choice to subscribe for the scheme and avail the benefit, which is disbursed in a maximum of 30 days. Because it benefits not just the insured but also the family of the EDLI member.

Grow your business with factoHR today

Focus on the significant decision-making tasks, transfer all your common repetitive HR tasks to factoHR and see the things falling into their place.

© 2026 Copyright factoHR