Payment of Gratuity Act, 1972: Eligibility, Calculation & Compliance Guide

Download Payment of Gratuity Act, 1972

Table of Contents

If you have worked in a company for five or more years in India, you are legally entitled to receive gratuity when you leave. And if you are an employer or HR professional managing a team of 10 or more employees, paying gratuity on time is not optional – it is a statutory obligation under the Payment of Gratuity Act, 1972.

This guide covers everything you need to know about the Act – who it applies to, when gratuity becomes payable, how to calculate it correctly, how the taxation works, and what happens when an employer delays or refuses payment.

What is the Payment of Gratuity Act, 1972?

The Payment of Gratuity Act, 1972, is a central labor law that governs how employers must pay gratuity to their employees. It came into force on 16 September 1972 and covers both government and private sector establishments.

Gratuity is a statutory lump-sum terminal benefit paid by an employer to an employee in recognition of long and continuous service. Unlike a bonus or incentive, it is not discretionary – every eligible employee has a legal right to claim it.

Which Establishments Does This Act Cover?

The Act applies to:

- Factories, mines, oilfields, plantations, ports, and railways

- Any shop or establishment with 10 or more employees on any day during the preceding 12 months

- Once the Act applies to an establishment, it continues to apply even if the employee count later falls below 10

The Act applies equally to public sector undertakings and private sector companies. It regulates gratuity payments and provides a legal mechanism for resolving disputes between employers and employees.

Who is Eligible to Receive Gratuity?

An employee becomes eligible for gratuity when any of the following conditions are met:

- The employee has completed five or more years of continuous service with the same employer (applicable at the time of resignation, retirement, or termination)

- The employee attains superannuation (retirement age) while in service

- The employee retires under the Voluntary Retirement Scheme (VRS)

Important: The 5-year minimum service condition is waived in cases of death or permanent disability. If an employee passes away or becomes permanently disabled, their nominee or the employee themselves can claim gratuity, regardless of how many years they have served.

What Counts as ‘Continuous Service’?

Under Section 2A of the Act, continuous service includes periods of authorized absence, leave with wages, lay-off periods, maternity leave, and any period during which an employee was absent due to temporary disablement caused by an accident or illness arising out of employment. It is not limited only to days actually worked.

Rules under the Payment of Gratuity Act, 1972

The Payment of Gratuity (Central) Rules, 1972, were framed under the Act and came into effect on 16 September 1972. Here are the key rules every employer and HR professional should know:

- Any establishment with 10 or more employees in the preceding 12 months must provide gratuity to eligible employees.

- Once the Act applies to an establishment, it continues to apply even if the employee count drops below 10 in subsequent years.

- Gratuity is not payable only at retirement – it is also payable on resignation (after 5 years), VRS, termination, retrenchment, death, and permanent disablement.

- The employer is solely responsible for paying gratuity. The employee does not contribute to it – unlike the Provident Fund.

- The employer must pay the gratuity amount within 30 days of it becoming payable. Delay beyond 30 days attracts interest.

- Employers must either take a group gratuity insurance policy from LIC or another approved insurer, or set up an approved gratuity fund to ensure they can meet this obligation.

How is Gratuity Calculated?

The gratuity amount depends on whether your establishment is covered by the Gratuity Act. There are two separate formulas.

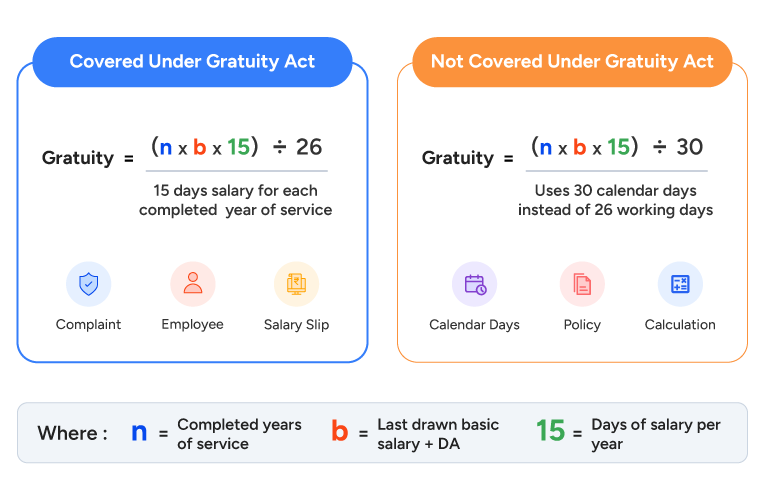

Formula 1: For Employees Covered under the Gratuity Act

Gratuity = (n x b x 15) ÷ 26

Where: n = completed years of service with the same employer, and b = last drawn basic salary plus dearness allowance (DA)

The denominator 26 represents the number of working days in a month (a calendar month has approximately 30 days, minus 4 Sundays). The formula effectively pays 15 days of salary for each completed year of service.

Worked Example

Ramesh has worked at a manufacturing company for 10 years. His last drawn basic salary plus DA is Rs. 45,000 per month.

Gratuity = (10 x 45,000 x 15) ÷ 26 = Rs. 2,59,615

Formula 2: For Employees Not Covered under the Gratuity Act

Gratuity = (n x b x 15) ÷ 30

Here, the denominator is 30 (calendar days in a month) instead of 26. All other variables remain the same.

How the 6-Month Rounding Rule Works

When calculating completed years of service, a partial year is handled as follows:

- If the remaining period is more than 6 months, it is rounded up to the next full year.

- If the remaining period is 6 months or less, it is ignored.

Example A: Service of 7 years and 7 months → counted as 8 years

Example B: Service of 7 years and 4 months → counted as 7 years only

What is the Maximum Gratuity Amount Payable?

The maximum gratuity amount that is legally enforceable under the Act is Rs. 20,00,000 (Rs. 20 lakh). This ceiling was revised upward from the earlier limit of Rs. 10 lakh.

If the calculated gratuity amount exceeds Rs. 20 lakh, the excess is treated as ex gratia – a voluntary payment by the employer. The employer is not legally required to pay the ex gratia portion, though many companies do so as part of their retention or reward policy.

Is Gratuity Taxable in India?

The tax treatment of gratuity depends on the employee’s category. There are three distinct categories under the Income Tax Act, 1961:

| Employee Category | Tax Treatment | Exemption Limit |

|---|---|---|

| Central/State Government employees and employees of local authorities | Fully exempt from income tax – no limit | No upper limit – entire amount exempt |

| Private sector employees covered under the Gratuity Act | Least of: (a) actual gratuity received, (b) Rs. 20 lakh, or (c) 15 days’ salary x years of service | Up to Rs. 20 lakh exempt; amount above Rs. 20 lakh taxed as income |

| Private sector employees NOT covered under the Gratuity Act | Least of: (a) actual gratuity received, (b) Rs. 20 lakh, or (c) half month’s average salary x completed years of service | Up to Rs. 20 lakh exempt (based on formula); balance taxable |

Note: Gratuity received in the event of death or permanent disablement is fully exempt from tax, regardless of the amount.

Nominating a Beneficiary Your Obligation under Section 6

One of the most overlooked compliance requirements under the Gratuity Act is the nomination process. Under Section 6, every employee who has completed one year of service must nominate a person who will receive the gratuity amount in case of the employee’s death.

This is done using Form F – the nomination form – which must be submitted to the employer. Key points to know:

- If the employee has a family (spouse, children), the nomination must be in favor of a family member.

- If the employee has no family at the time of nomination, they can nominate any person. However, if they subsequently acquire a family (e.g., after marriage), the earlier nomination in favor of a non-family member becomes invalid.

- The employer is responsible for maintaining nomination records and ensuring they are kept up to date.

- If no nomination is made and the employee dies, the gratuity is payable to the employee’s legal heirs.

How to Claim Gratuity Step by Step Process

If you are an employee who has become eligible for gratuity, here is how you claim it:

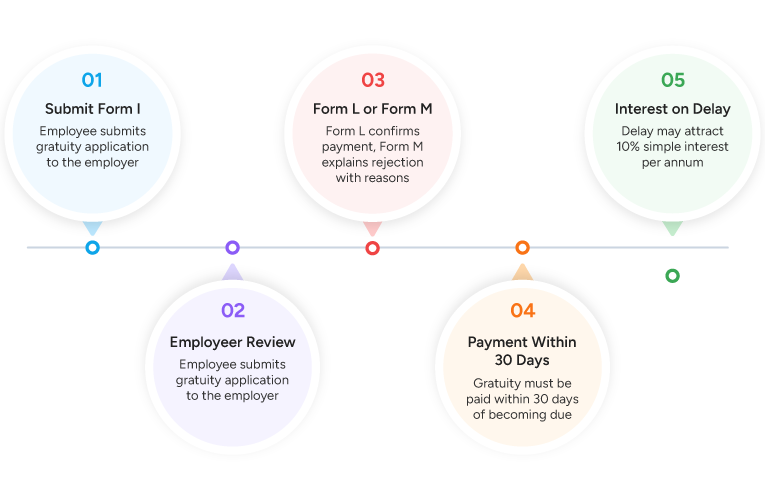

- Submit Form I (Application for Gratuity by Employee) to your employer. This form contains your personal details, service period, and the gratuity amount you are claiming.

- The employer must acknowledge your application and issue Form L (Notice of Payment of Gratuity) within 30 days, stating the gratuity amount payable.

- If the employer disputes the amount or eligibility, they must issue Form M (Notice Rejecting Application) with written reasons.

- Gratuity must be paid within 30 days of it becoming due. If the employer fails to pay within this period, they are liable to pay simple interest at 10% per annum on the outstanding amount from the due date.

- In case of the employee’s death, the nominee must submit Form J (Application for Gratuity by Nominee) instead of Form I.

What Happens if an Employer Delays or Refuses to Pay Gratuity?

The Act is clear: gratuity must be paid within 30 days of its becoming payable. If your employer does not pay on time, here is what you can do:

- Send a written reminder to your employer citing your legal right under the Gratuity Act.

- If there is no response, send a legal notice through an advocate.

- File a complaint with the Controlling Authority (typically the Assistant Labor Commissioner or Regional Labor Commissioner in your district). The Controlling Authority has the power to direct the employer to pay the gratuity along with interest.

- If you are dissatisfied with the Controlling Authority’s decision, you can appeal to the Appellate Authority within 60 days.

Penalty for Non-Payment

An employer who knowingly fails to pay gratuity may face imprisonment of not less than 6 months, extendable to 2 years, a fine, or both. Simple interest at 10% per annum is payable for any delay beyond 30 days.

When Can an Employer Forfeit Gratuity?

In limited circumstances defined under Section 4(6) of the Act, an employer can forfeit all or part of the gratuity. There are two distinct situations:

Partial Forfeiture

If an employee’s services are terminated because of wilful omission or negligence that causes damage or loss to the employer’s property, the employer may forfeit gratuity to the extent of the damage. For example, if an employee’s negligence caused damage to machinery valued at Rs. 50,000, the employer can deduct up to Rs. 50,000 from the gratuity amount.

Full Forfeiture

If the employee’s services were terminated for riotous or disorderly conduct, workplace violence, or any offense involving moral turpitude (a legally defined term under Indian law for serious criminal offenses), the entire gratuity may be forfeited.

It is important to note that simple misconduct, poor performance, or violations of general workplace policies do not automatically justify forfeiture. Forfeiture is a serious legal step and must be backed by a proper disciplinary process and termination order.

What the New Labor Codes Mean for Gratuity

The Code on Social Security, 2020 – one of the four new Labor Codes – will consolidate the Payment of Gratuity Act, 1972, along with several other social security laws, into a single statute once it is notified and brought into force by the government.

While the core provisions of gratuity remain largely unchanged in the Code, HR and payroll professionals should note a few forward-looking changes:

- Understanding gratuity rules under new labour laws is important because fixed-term employee eligibility, wage definitions, and gratuity calculations may directly affect payroll planning and statutory compliance.

- Fixed-term employees will be entitled to pro-rata gratuity even if they have not completed five years of service. This is already applicable in some sectors and will be broadened.

- The definition of ‘wages’ for gratuity calculation may change under the new Codes, potentially impacting how basic salary is computed.

- Once the Codes are notified, the Payment of Gratuity Act, 1972, will cease to operate as a standalone law.

As of now, the Payment of Gratuity Act, 1972, remains fully in force. Please keep track of updates from the Ministry of Labor and Employment for notification dates.

Conclusion

The Payment of Gratuity Act, 1972, is one of India’s most important employee protection laws. Whether you are an employee planning your retirement or an HR professional managing compliance, understanding how gratuity works – from eligibility and calculation to taxation and claims – is not just good practice, it is a legal requirement.

If your organization is managing gratuity manually, errors in calculation, missed deadlines, and incorrect tax treatment can lead to penalties and employee grievances. An HRMS like factoHR automates gratuity calculations, maintains nomination records, generates necessary forms, and ensures you remain compliant – without the administrative burden.

Frequently Asked Questions

Does the Gratuity Rule Differ for Private Sector Employees?

No. The same Payment of Gratuity Act, 1972, applies to both public and private sector employees. The formula, eligibility conditions, and maximum limits are identical. The only difference is in the income tax treatment: government employees get a full exemption, while private-sector employees have a cap of Rs. 20 lakh on their exemption.

Is Gratuity Deducted from an Employee’s Monthly Salary?

No. Gratuity is entirely funded by the employer. It is not deducted from your CTC or monthly salary. The employer bears the full cost and is required to either take a group gratuity insurance policy or create an approved gratuity trust fund to meet this obligation.

Who Receives the Gratuity Amount if the Employee Passes Away?

The gratuity is paid to the nominee named in Form F. If the employee has nominated a family member (spouse, children, parents), the payment goes to them. If no nomination has been made, the amount is paid to the employee’s legal heirs. The employer must settle the payment promptly and cannot delay it.

Is Gratuity Payable before Completing 5 Years of Service?

Yes – in two specific situations. If an employee passes away during service or suffers permanent disablement due to an accident or illness, gratuity is payable regardless of how many years they have served. This is one of the most critical provisions that many employers overlook, and non-payment in such cases constitutes a violation of the Act.

Is the Gratuity Amount the Same for all Employees?

No. The gratuity amount varies for each employee because it is calculated based on their last drawn basic salary plus DA and their total years of service. An employee with a higher salary and longer service will receive a higher gratuity amount.

Can an Employee be Denied Gratuity Even after Completing 5 Years?

An employer can forfeit gratuity only under Section 4(6) of the Act – specifically, if the employee was terminated for wilful negligence causing damage to property (partial forfeiture), or for an offense involving moral turpitude or violent/riotous behavior (full forfeiture). General poor performance or policy violations are not valid grounds for forfeiture.

What is the Last Date to Claim Gratuity after Leaving a Job?

You should apply for gratuity (using Form I) on or before the date of separation, or as soon as possible thereafter. While the Act does not prescribe a strict limitation period for the employee’s application, it is best practice to apply promptly. The employer, on their part, must pay within 30 days of the gratuity becoming due, whether or not the employee has formally applied.

Grow your business with factoHR today

Focus on the significant decision-making tasks, transfer all your common repetitive HR tasks to factoHR and see the things falling into their place.

© 2026 Copyright factoHR