Advance Tax: Meaning, Importance & Calculation (2026 Guide)

Table of Contents

Paying taxes regularly is an act of responsibility. As incomes rise and financial activities diversify, the need for timely tax planning is taking center stage.

Advance tax payment, oftens overlooked by individuals and businesses alike, plays a vital role in ensuring tax compliance and avoiding unnecessary interest charges.

This guide explains the meaning of advance tax, its applicability, calculation method, due dates, penalties for delay, and more. Whether the income comes from salary, business, rent, capital gains, or professional fees, this 2025 guide covers all aspects of advance tax calculation and payment.

What is Advance Tax?

Advance tax is income tax paid in installments throughout the financial year, following the “pay-as-you-earn” model, where tax is paid in part on income earned during the year.

Advance Tax Applicability:

It applies to individuals, professionals, businesses, freelancers, and Non-Resident Indians (NRIs) when their total tax liability in a financial year exceeds ₹10,000. This system ensures steady government revenue that aids in the smooth functioning of crucial government sectors.

It also helps distribute the taxpayer’s burden and supports better financial planning by avoiding large year-end payments. If advance tax is not paid according to the schedule, interest is charged under the relevant sections in addition to the tax due.

Why does Advance Tax Exist?

The government requires a steady income throughout the year to fund public services, infrastructure, and welfare programs. Advance tax helps maintain this steady flow by collecting income tax in installments instead of a single lump sum payment at year-end.

The legal framework for advance tax is defined under Sections 208 to 219 of the Income Tax Act. These sections explain the rules and procedures for advance tax payments, including the applicability of paying tax in advance, due dates, and the penalty for late payments.

Advance tax also benefits taxpayers. Paying taxes in installments reduces the year-end financial burden, improves cash flow, and lowers the risk of missing deadlines or incurring penalties.

Who has to Pay Advance Tax?

Advance tax is not limited to just business owners; salaried individuals, freelancers, professionals, and even non-residents may be required to pay it. Based on the type of income and taxpayer category, paid tax rules may differ.

Besides this taxes, salaried and self-employed individuals are required to pay professional tax in India, which is a state-level tax.

Below are the key groups required to pay advance tax:

1. Individuals & Salaried Employees

Salaried employees are required to pay advance tax if their tax liability exceeds ₹10,000 in a financial year after adjusting TDS or TCS. This usually happens when they have additional sources of income, such as:

- Interest from fixed deposits

- Rental income

- Capital gains

- Earnings from the lottery or other winnings

Even though employers deduct TDS or TCS, salaried individuals with other income must calculate their total tax liability and pay the shortfall as advance tax.

2. Businesses & Professionals

Advance tax applies to self-employed individuals and businesses, including:

- Professionals like doctors, lawyers, architects, and consultants

- Freelancers and gig workers who earn income outside of traditional employment

- Businesses, whether small or large

- Non-resident Indians (NRIs) who earn income in India and meet the tax threshold

- Companies and partnership firms operating in India with taxable profits

Taxpayers under presumptive taxation (Sections 44AD (for small businesses) and 44ADA (for professionals)) must pay 100% of their advance tax by 15th March in a single installment instead of quarterly payments.

3. Exemptions

Advance tax is not applicable in the following cases:

- Senior citizens (aged 60 years or above) who do not earn income from business or profession

- Individuals who earn only agricultural income

- Cases where the total tax liability is ₹10,000 or less in a financial year

These exemptions are in place to reduce the compliance burden for low-income and retirement-age taxpayers.

Advance Tax Calendar FY 2025-26 (Assessment Year 2026-27)

The advance tax payment dates are as follows:

| Installment | Due Date | % of Total Tax | Note |

|---|---|---|---|

| 1st | 15 Jun 2025 | 15% | Since 15 Jun 2025 falls on a Sunday, you can pay advance tax by 16 Jun without interest |

| 2nd | 15 Sep 2025 | 45% (cumulative) | Includes the first installment; non-payment may attract interest under Section 234C |

| 3rd | 15 Dec 2025 | 75% (cumulative) | Shortfall leads to interest under Section 234C |

| 4th | 15 Mar 2026 | 100% | Final installment; no concession for weekends |

Note:

No interest under Section 234C will be charged if advance tax is paid up to 12% by the first installment and 36% by the second installment of the total tax liability.

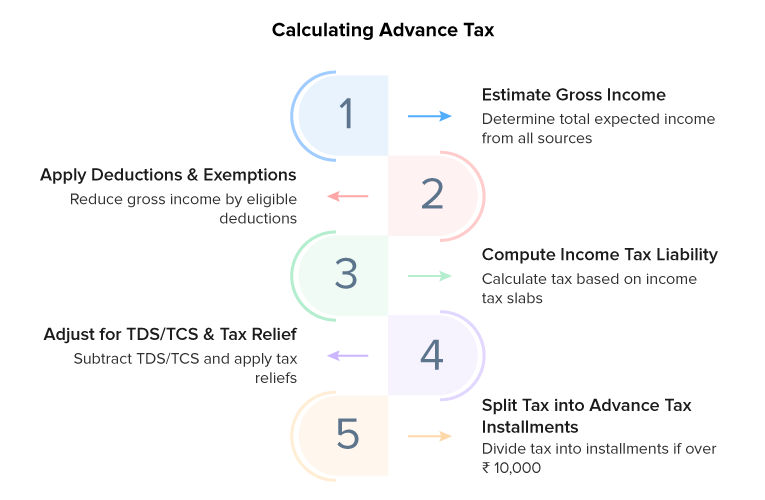

How to Calculate Your Advance Tax

Calculating advance tax helps avoid interest and penalties. The process is easy when broken down into clear steps:

Step 1: Estimate Gross Income

Start by estimating the total income expected during the financial year. This includes all sources such as:

- Salary income. Payroll taxes are levied on the wages or salaries paid by employers to their employees

- Business or professional income

- Capital gains from selling shares, property, or mutual funds

- Interest from fixed deposits (FDs), savings accounts, or recurring deposits

- Income from cryptocurrencies or digital assets

If the income includes salary, use the employer’s income projection. For freelancers and business owners, refer to past income trends and current contracts or deals.

Step 2: Apply Deductions & Exemptions

Next, reduce the gross income by applying eligible deductions and exemptions. These reduce the taxable income. Some common deductions under the Income Tax Act include:

- Section 80C: Investments in PPF, ELSS, LIC, etc. (Up to ₹1.5 lakh)

- Section 80D: Health insurance premiums

- House Rent Allowance (HRA): If staying in rented accommodation

- Education loan interest: Under Section 80E

- Home loan interest: Under Section 24(b)

Step 3: Compute Income Tax Liability

Now, calculate the tax liability after deductions:

- Apply the relevant income tax slab rates.

- Add a surcharge if income exceeds the prescribed limits.

- Add 4% health and education cess on the total tax.

This gives the total income tax payable for the year.

Step 4: Adjust for TDS/TCS & Tax Relief

If Tax Deducted at Source (TDS) or Tax Collected at Source (TCS) has already been deducted, subtract it from the total tax liability.

Also, subtract any foreign tax credits or other applicable reliefs.

Example: If the total tax is ₹60,000 and the TDS already paid is ₹20,000, then the balance tax = ₹40,000.

Step 5: Split Tax into Advance Tax Installments

If the final tax payable after TDS exceeds ₹10,000, advance tax must be paid. Divide it as per the advance tax schedule mentioned in the advance tax calendar for the 2025-2026 table.

Example: Advance Tax Calculation for Freelance Graphic Designer Ravi

Advance tax for freelancers like Ravi is calculated with the following annual income:

Total Gross Income:

- Professional income: ₹8,00,000

- Interest income (FD): ₹50,000

- Capital gains: ₹1,50,000

- Total gross income: ₹10,00,000

Deductions:

- Section 80C (PPF investment): ₹1,50,000

- Section 80D (Health insurance): ₹25,000

- Net taxable income: ₹8,25,000

Tax Calculation:

- Tax on ₹8,25,000 (based on the old regime): ₹72,500

- Add 4% cess: ₹2,900

- Total tax liability: ₹75,400

- TDS deducted by bank: ₹5,400

- Advance tax payable: ₹70,000

Note:

The tax liability in the above example is calculated under the old tax regime, as deductions under Section 80C are more beneficial to the assessee. These deductions are only available under the old regime.

Installments:

| Installment | % of Tax | Amount | Due Date |

|---|---|---|---|

| 1st | 15% | ₹10,500 | 15 Jun 2025 |

| 2nd | 30% | ₹21,000 | 15 Sep 2025 |

| 3rd | 30% | ₹21,000 | 15 Dec 2025 |

| 4th | 25% | ₹17,500 | 15 Mar 2026 |

This process helps in accurate advance tax calculation and avoids late payment interest.

Interest & Penalties for Shortfall or Late Payment

Paying advance tax on time is essential. If a person misses the deadline or pays less than the required amount, the Income Tax Department charges an advance tax penalty. This interest is charged under Sections 234B and 234C of the Income Tax Act.

Section 234B – Interest for Non-Payment or Shortfall

This section applies when:

- Advance tax is not paid at all, or

- Less than 90% of the total tax liability is paid as advance tax.

Interest Charged:

1% interest per month (or part of a month) is charged on the outstanding tax amount from 1st April until the date of actual payment.

Example:

Suppose an assessee has a total tax liability of ₹60,000 for the financial year. They pay only ₹50,000 as advance tax by 31st March. The remaining ₹10,000 is paid later on 15th September during the filing of the income tax return.

As per Section 234B, the interest will be charged as follows:

- Shortfall = ₹10,000

- Period of delay = April to September = 6 months

- Interest = ₹10,000 × 1% × 6 = ₹600

Therefore, the assessee will be required to pay ₹600 as interest under Section 234B in addition to the pending amount of ₹10,000.

Section 234C – Interest for Late or Uneven Installment Payments

This section applies when advance tax is paid after the due dates or not in the correct proportions.

| Installment Due | Advance Tax Due | Interest Charged (if shortfall) |

|---|---|---|

| 15 June | 15% of total tax | 1% per month for 3 months |

| 15 September | 45% (cumulative) | 1% per month for 3 months |

| 15 December | 75% (cumulative) | 1% per month for 3 months |

| 15 March | 100% | 1% for 1 month |

Example:

Let’s assume a taxpayer was required to pay ₹15,000 as the first installment of advance tax by June 15, but the payment was delayed and made on July 15.

As per the rule, if advance tax is not paid on time (even if the delay is by just one day), interest will be calculated as follows:

- Shortfall = ₹15,000

- Interest rate = 1% per month

- Interest period = 3 months (as per Section 234C rule)

- Interest = ₹15,000 × 1% × 3 = ₹450

Therefore, the taxpayer will be required to pay ₹450 as interest under Section 234C in addition to the ₹15,000 installment amount.

To avoid penalties, it’s best to use an advance tax calculator and pay in the correct installments.

Step-By-Step: Paying Advance Tax Online

Advance tax can be paid easily through the e-Pay Tax portal (TIN 2.0) on the Income Tax Department’s official website.

Here’s how:

Step 1: Visit the E-Filing Portal

Advance tax payment online can be done by logging into the official Income Tax e-filing portal. Click on “e-Pay Tax”under the Quick Links section on the homepage. It can also be accessed by searching “e-Pay Tax” in the search bar.

Step 2: Enter PAN Details

Enter PAN, confirm it, and then enter the mobile number linked with the account. Click “Continue.”

Step 3: Verify with OTP

Enter the 6-digit OTP sent to your mobile number and click “Continue.”

Step 4: Select ‘Income Tax’ as the Tax Type

On the “New Payment” page, choose the first box: ‘Income Tax (Other than Companies)’ and click “Proceed.”

Step 5: Choose Assessment Year & Payment Type

- Assessment Year: Select 2026–27 (for FY 2025–26)

- Type of Payment: Choose ‘Advance Tax (100)’ Click “Continue.”

Step 6: Enter Tax Amount

Fill in the tax amount to be paid under ‘Advance Tax.’

Step 7: Select Payment Method

Choose your payment method (Net Banking, Debit Card, UPI, or other options). Select the bank and click “Continue.”

Step 8: Review & Pay

Verify the challan details and click “Pay Now.” If anything needs correction, click “Edit.”

Step 9: Save the Receipt

Once payment is complete:

- An acknowledgment will appear.

- The BSR Code and Challan Serial Number can be seen on the right.

- Save this receipt. It is required when filing the ITR and for reconciling with Form 26AS and AIS.

Step 10: Reconciling in Form 26AS and AIS

After payment, it is essential to verify that the amount has been credited correctly.

Form 26AS:

This is a tax credit statement available on the Income Tax portal. It reflects TDS, advance tax, and self-assessment tax. Ensure your advance tax appears here with the correct BSR code and challan number.

AIS (Annual Information Statement):

The AIS also shows advance tax payments. It helps in matching the data before filing returns.

If the tax paid is missing or incorrect in these statements, contact the bank or the IT department to resolve the issue.

Advance Tax for Special Cases

Different advance tax rules apply based on the taxpayer’s income type or category.

Here’s how it applies in special cases:

Presumptive Taxation (Sections 44AD, 44ADA, 44AE)

Under the presumptive taxation scheme, eligible small businesses and professionals can estimate their income and pay tax accordingly without maintaining detailed books.

- Section 44AD: For eligible businesses

- Section 44ADA: For professionals like doctors, lawyers, etc.

- Section 44AE: For transport businesses owning goods vehicles

Under this scheme, advance tax must be paid in a single installment by March 15 of the financial year. Failure to do so may result in interest under Sections 234B and 234C.

Capital Gains

Advance tax on capital gains (e.g., from selling property or stocks) is payable in installments after the gain is realized. For example, if a capital gain occurs in November, tax on it must be included in the next due installment (15th December or 15th March). Non-payment attracts interest under Section 234C.

Senior Citizens

Resident senior citizens (aged 60 or above) are exempt from paying advance tax if they do not have income from business or profession. This exemption is provided under Section 207 of the Income Tax Act.

Income from pension, fixed deposit interest, or rental sources does not affect this exemption. In simple terms, if the senior citizen earns from these passive sources and not from a business or profession, the Tax paid in advance for senior citizens is not applicable.

NRIs (Non-Resident Indians)

Advance tax for NRIs applies if their total tax liability exceeds ₹10,000 for the financial year. NRI income arising from renting Indian property, capital gains, or business income generated in India is taxable in India. NRIs can pay their tax in advance online via the e-Pay Tax portal, just like resident taxpayers. The payment must be made in INR, and the correct PAN details should be entered to ensure proper credit.

How to Check Advance Tax Payment Status

After paying advance tax, it’s essential to verify whether the payment has been credited to the Income Tax Department.

Taxpayers can easily check the status of their tax deduction before year-end payments using the TIN-NSDL (OL-TAS) portal. The portal offers two convenient search options:

CIN-Based View (Challan Identification Number)

- Go to the TIN-NSDL Challan Status Enquiry page.

- Click on “Challan Status Inquiry” and select “CIN Based View”.

- Enter the required details:

- BSR Code of the bank branch

- Date of deposit

- Challan serial number

- Amount (optional)

- The system will display:

- BSR code

- Deposit date

- Challan serial number

- Major Head Code and description

- PAN/TAN

- Taxpayer’s name

- Date of receipt by TIN

- Confirmation of the correct amount (if entered)

TAN-Based View (Tax Deduction and Collection Account Number)

- Select “TAN-Based View” on the same portal.

- Enter:

- TAN

- Challan tender date range for the financial year

- You will be able to view:

- CIN

- Major/Minor Head Codes

- Nature of payment

- System confirmation if the entered amount matches bank records

This feature helps ensure your advance tax has been received and correctly recorded by the Income Tax Department.

Corrections & Refunds in Advance Tax

Sometimes, when paying advance tax, errors may occur, such as selecting the incorrect assessment year, entering an incorrect PAN, or choosing the wrong payment method. These mistakes can affect the tax credit reflection and may even result in notices from the department. Fortunately, the Income Tax Department permits corrections and refunds subject to certain conditions.

How to Correct Errors in Advance Tax Challan

If there’s an error in:

- PAN number

- Assessment year

- Major/minor head of payment

- Payment type (e.g., self-assessment tax vs. advance tax)

You can request a correction by following these steps:

- Visit your bank branch where the payment was made (within 7 days for minor changes).

- Submit a Challan Correction Request with:

- Copy of the original challan

- PAN proof

- Written application

- For major corrections, log in to the Income Tax e-filing portal and:

- Go to Services > Challan Correction Request

- Select the relevant challan and submit the correction.

- Alternatively, the jurisdictional Assessing Officer can be contacted through the portal under the “Grievances or Requests” section.

Time Limit: Corrections can usually be made within 7 days at the bank or up to 12 months via the e-filing portal, depending on the nature of the error.

How to Claim Refund for Excess Advance Tax Paid

In case more advance tax is paid than the actual tax liability:

- File the income tax return within the due date.

- Ensure the excess payment is clearly visible in Form 26AS.

- The IT Department will process the refund after the assessment is complete.

- Refunds are usually credited directly to the bank account linked with the PAN.

Track your refund status via:

- TIN NSDL Refund Status Portal

- Or through the Income Tax portal > Services > Refund Status

Note: Timely correction and refund claims ensure smooth tax credit matching and avoid legal or financial complications later.

Conclusion

Paying advance tax on time helps avoid a significant tax burden at the end of the year, reduces the risk of interest and penalties, and gives better control over finances. It also ensures that the government receives a steady flow of funds, which supports national development.

Whether one is a salaried employee, freelancer, business owner, or NRI, comprehending the mechanics of prepaid tax can significantly influence financial planning. If you’re unsure about how to declare your taxes properly, check out our guide on income tax declaration challenges to avoid common mistakes.

Using tools like an advanced tax calculator can help you estimate the right taxable amount. But if you want to be truly stress-free, it’s best to consult a tax expert or use trusted software. factoHR is a trusted name in the industry with smart, user-friendly solutions for payroll, tax declaration, and compliance. This HR software is everything you need to stay timely, accurate, and confident during tax season. Make tax season easier with factoHR by your side. Book a free trial right away!

FAQs

Is Advance Tax Mandatory for Salaried Employees?

Yes, if the total tax liability (after TDS or TCS) exceeds ₹10,000 in a financial year.

Can Advance Tax Payments be Revised Later?

Yes, the remaining installments can be adjusted based on updated income estimates.

Do Senior Citizens have to Pay Advance Tax?

No, senior citizens (60 years and above) who do not have business income are exempt from this requirement.

What if Income Reduces after Paying Tax in Advance?

Any excess tax paid will be refunded after filing the income tax return.

Is Advance Tax Applicable on Lottery or Casual Income?

Yes, such incomes are taxable, and advance tax must be paid if the total tax liability crosses ₹10,000.

Who Needs to Tax in Advance?

Individuals, businesses, professionals, freelancers, and NRIs whose estimated annual tax is more than ₹10,000 need to pay tax.

What Happens if the Advance Tax is Not Paid?

Interest is charged under Sections 234B and 234C for non-payment or shortfall.

How is Advance Tax Different from Self-Assessment Tax?

Tax is paid during the year on estimated income. Self-assessment tax is paid after the end of the financial year before filing the return.

Can Prepaid Tax be Paid after the Due Date?

Yes, but interest will be charged for late payment.

How do I Calculate Advance Tax on Capital Gains?

Estimate the gain, compute the tax, and pay it in the next due installment. Use an advanced tax calculator for accurate computation.

Grow your business with factoHR today

Focus on the significant decision-making tasks, transfer all your common repetitive HR tasks to factoHR and see the things falling into their place.

© 2026 Copyright factoHR